How does an organization ensure it is prepared to minimize losses and recover quickly following a natural disaster? Long before a disaster strikes and property damage occurs, the best response plans begin with careful negotiation and placement of well-defined property coverage. Advanced knowledge of technical insurance terms and contract language is important in determining both coverage and exclusions. In addition, it is critical to have a carefully crafted loss prevention plan in place to ensure the organization is prepared to spring into action as soon as an incident occurs.

Key Considerations for Disaster Planning

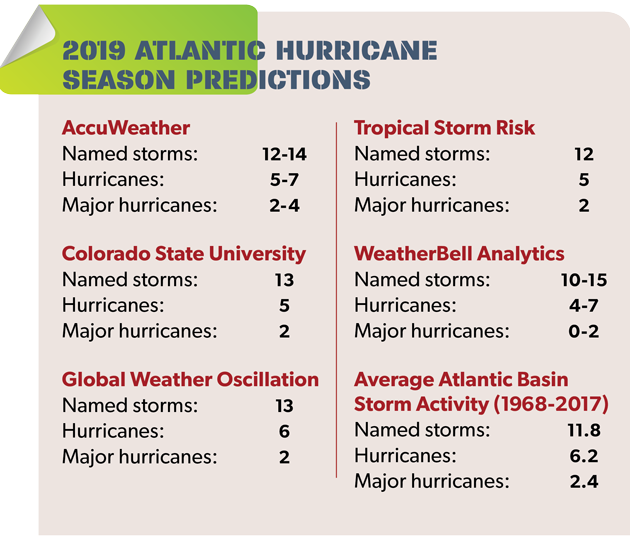

Larger storms mean bigger headaches for businesses and their employees. Meticulous disaster response planning has therefore never been more important. When developing a plan, it is important to involve key stakeholders and review every step that your business, your network and your vendors must take if a natural catastrophe impedes operations. A strong plan should address these key questions. Read more in Key Considerations for Disaster Planning.

Deploying and managing the right resources at the right time is both an art and a science. By understanding how to prepare for and respond to a catastrophe, you can ensure the smoothest possible recovery for your business.

Pre-Event Preparation

When a catastrophe or natural disaster occurs, potential property claims can be significant. Immediate response is critical—the longer the response time, the greater the financial risk to an organization in terms of property damage, business interruption and economic loss.

First, it is critically important for organizations to understand their risk exposure in advance of a catastrophe. Most businesses will have a variety of insurance policies to protect them from different types of loss, such as:

- Property policies to cover property damage and loss

- Business interruption insurance to protect against loss of income due to an inability to conduct business

- Contingent business interruption protection to cover the physical damage to a supplier or customer that impacts an organization’s ability to conduct business

- Liability insurance to protect the business in the event of a legal suit

Simply having insurance is not enough. A company must secure insurance policies that are broad enough to cover business needs and know how these policies work and what coverage they provide.

Businesses should meet with their insurance agents or brokers on an annual or semi-annual basis to ensure coverage is up to date and reflects any change in operations or exposures. Insurance agents and brokers should be notified immediately of any property purchases or sales, adding or deleting these locations from the insurance property schedule to ensure adequate coverage is in place.

Businesses should also meet with their claims administrator to explain business operations and review coverages. All parties should understand coverage terms and conditions and know how the policy would be applied in the event of a loss. A lack of adequate coverage for a loss can be devastating, leading to delays in recovery and restoration and magnifying the impact of the disaster.

Multinational companies must understand the insurance laws in each jurisdiction in which they operate and how these regulations impact their coverage and emergency response. Having quality partners who can provide local expertise, ground personnel and technical support is key to mitigating loss. In order to avoid underinsurance issues—which can be common in certain regions—companies need to work with qualified brokers, carriers and claims administrators to understand policies, coverage and exclusions before disaster strikes because, once damage occurs, only the policy provisions in force will be applied.

Establishing an Emergency Response Plan

A properly-designed emergency response plan is essential to reduce damage-related costs and speed recovery. The plan should outline appropriate actions to be taken by both internal and external resources. A qualified loss prevention and safety specialist can be beneficial in developing an effective plan that considers both internal business policies and local regulations. The plan also should reflect established partnerships with reliable contractors and other service partners needed for damage control and recovery efforts. It is important to consult with all vendor partners when developing the plan to ensure that all facets of business operations and exposures are addressed.

One of the most important components of a disaster recovery plan is assembling an emergency response team that will be responsible for creating, monitoring and implementing the plan when necessary. All team members should be aware of how to access the plan at all times and should actively ensure it remains current and up to date.

In general, emergency response planning should address:

- Physical risk mitigation. Determine how to protect physical property and other assets from potential damage, including ensuring the building or facility is structurally sound and can withstand a storm, earthquake or fire.

- Business recovery. Develop a detailed plan that addresses how to maintain and restore business operations, both during and after a disaster. This should include assessing and documenting all assets, including current inventory records, tax records, receipts, and video showing the property layout and types of items at the property prior to a loss.

- Emergency response plan implementation. Establish clearly defined communication procedures, checklists, protocols and equipment to be used in executing the plan in the event of emergency. This includes identifying emergency response team members and specifically dedicating time to testing the plan’s effectiveness.

- Securing the site. Document the steps to be taken as soon as practical after an event to ensure the site is secure, safety requirements have been met and, if necessary, operations have been safely shut down. This portion of the plan should include the location of all utilities and main cut-off locations.

- Business interruption. Develop a plan for temporary restoration of business operations. This might include outsourcing of services, using an alternative worksite, or leasing additional equipment. The plan should include some redundancies across worksites to ensure that business activity can be transferred or resumed as necessary.

- Site clean-up and repair. Create a plan to remediate property damage, including a list of reliable contractors and services to begin restoration as quickly and efficiently as possible.

- Filing a claim. Outline the procedures to initiate a claim and have insurance broker and loss adjuster contact information readily accessible to emergency response team members.

There is no one-size-fits-all response plan for all companies. Key items need to be tailored to actual business needs and risk exposure. An effective plan will consider pre-event staffing and risk partners, identifying exposures, emergency training and drills, defining protocols, and establishing the use of emergency notification systems and other relevant technologies.

Prior to an event, business leaders should provide as much exposure information as possible to the emergency response team. They should take precautions to inspect and protect the property and make sure routine safety checks and maintenance are completed. Keeping good records of all safety checks and maintenance can help ensure the company is prepared to weather even the most disruptive event.

Multinational businesses need to consider how insurance policies and regulations vary from country to country and take steps to have local expertise in place. They must have a broad representation of talent on their emergency response teams and team members should be located in different areas when possible. For example, companies who have all billing, human resources or other support services at a single physical site will be at significant risk of interrupted operation if that location suffers a loss.

During an Event

While one can never fully predict the impact of a natural disaster, with a solid emergency plan in place, businesses will be prepared to respond quickly and effectively when disaster strikes.

Generally, an initial impact assessment can be made during or immediately following an event, and can help guide the course of action. In the event of a significant windstorm or blizzard, business leaders can determine if and when operations will need to be shut down or when employees should be sent home.

An effective emergency plan will outline communication procedures for notifying employees, customers, emergency services and other key stakeholders in the event of a natural disaster, and this should encompass multiple modes of communication in the event telephone, electric or mobile services are unavailable. It will be up to the emergency response team to ensure that all pre-determined tasks are carried out at each warning stage of the event.

After an Event

When a catastrophe strikes, communities can be devastated and insurers may face a staggering number of claims. The goal of all parties is to get communities and businesses back on their feet as quickly as possible. Companies should make note of friction points during and after events to update and improve emergency response plans for the future.

In the planning process, companies should establish relationships with trusted contractors, surveyors, construction engineers, plumbers, electricians, and experts in drainage and asbestos removal to be called upon immediately when needed. In the aftermath of a disaster, these relationships can help ensure that damage will be repaired and operations restored as quickly as possible. Experienced loss adjusters can help manage the mitigation process and provide access to needed service partners. This third-party approach provides businesses with peace of mind that services are being managed and can drastically reduce project duration and costs.

Whether a company chooses to work with vendors directly or use a third-party approach, it is critical to establish vendor relationships and service expectations before a disaster strikes. Similarly, it is important to identify resources for replacing essential business equipment and establishing off-site locations or alternative supply chains, if needed.

Businesses also need to evaluate emergency response plans on an ongoing basis. Regular review and practice drills can help ensure that plans will be successful.

As the threat of natural disasters continues to grow, organizations must understand their risk exposure and plan accordingly so they can be confident that they will be able to weather virtually any storm.